Starting from mid-August, the price of fuel in Ukraine has increased by more than UAH 3. As a result, the average price of gasoline A95 in early October exceeded UAH 33. Such an increase in prices troubled consumers and led to protests. Protestants accused the gas station of conspiracy and the state of too high taxes. In fact, the key factors behind price growth have been the rise in oil prices in world markets and devaluation of hryvnia. The margin of the gas station is relatively small and stable, and the level of taxes in the price structure is lower than in the EU countries. An indirect factor affecting the price is the increase in smuggling and the number of illegal gas stations. Combined with the general trend of reducing fuel consumption in Ukraine, indirect factors adversely affect the financial position of key players in the market.

Key factors determining the price of fuel in Ukraine

The increase in fuel prices in early October 2018 was primarily driven by rising of oil prices and lowering the hryvnia exchange rate. Most of the fuel in Ukraine is imported. Supplies of imported gasoline are paid in currency, so retail fuel prices are very sensitive to changes in the hryvnia exchange rate. At the same time, the strengthening of the hryvnia rate does not lead to a rapid reduction in the price of fuel. Part of the taxes on fuel, namely the excise import tax, is fixed in Euros. From 1 liter of gas A 95 we pay 0.213 euros of import excise tax.

Starting from mid-August, the price of oil on world markets has grown by 15%. In turn, since mid-July, the hryvnia has fallen in price relative to the USD and Euro by about 7% (about +2 hryvnias). These two trends – rising oil prices and lowering the hryvnia exchange rate – led to rising of fuel prices in Ukraine. The growth of the purchase price of petroleum products by 1% causes a rise in the price of one liter for UAH 0.1 , while a decrease in the national currency exchange rate by UAH 1 leads to a rise in the cost of 1 liter of fuel by UAH 0.7-0.8. In this way, we will receive UAH 3, which has increased the retail price.

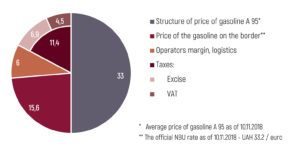

The share of petrol stations in fuel price structure is relatively insignificant and stable. According to various estimates, it ranges from 7 to 14% depending on the brand. Also up to 5-6% are logistics costs. Taxes account for a much larger share – 35%, and the actual purchase price of imported gasoline – 47%. These two components are directly dependent on the hryvnia exchange rate.

Indirect factors of influence on the price of fuel

Indirect impact on the price and financial position of key players is unfair competition, which reveals in the form of growth of the illegal distribution network. Without tax burden, and the costs of network development, illegal operators sell fuel at UAH/l 6-7 cheaper than legal ones. Their number reached 1.5 thousand. Illegal sales points of fuel cover 15-17% of sales of Diesel and 30-50% of LPG.

In addition, the volume of smuggling is increasing. Today, the main scheme of smuggling is the delivery of aviation fuel. Supplies of aviation fuel are one and a half times higher than the needs of Ukrainian airports. 30% of the imported air fuel is mixed with Diesel. The reason for the distribution of this scheme is due to the peculiarities of taxation. The excise tax rate on fuel oil is seven times lower than diesel. Thus, the “economy” of the excise tax is € 100 / thousand liters.

For 8 months of this year, the amount of aviation fuel that was not sent to airports was 160 thousand tons. According to expert estimates, the state lost about 950 million USD of unpaid excise tax. The main volume of aviation fuel for these needs comes from the port in Nikolaev. However, the tax service refuses to notice it.

As a result, legal operators reduce sales, and costs remain unchanged. When trying to keep profitability on smaller volumes, they can not react as quickly as unscrupulous competitors to changing market conditions.

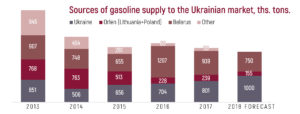

An additional risk factor for the Ukrainian fuel market may be its dependence on imports from Belarus. Belarus received from Russia several times more oil and petroleum products than consumed by itself. The surplus was re-exported, including in Ukraine. Such a scheme existed due to preferential taxation of oil imported from Russia to Belarus. However, in early September 2018, Energy Minister of the Russian Federation, Alexander Novak, said that the export of Russian oil products to Belarus is economically inappropriate. It is planned to establish a maximum level of supply of petroleum products from Russia to Belarus in 2019 (indicative balance), deliveries beyond these volumes will be restricted. In this case, a situation may arise when the Belarusian refinery will be in a difficult position to obtain oil for processing in order to satisfy the demand of the Ukrainian side.

However, a number of experts believes that in case of strengthening Minsk’s conflict with Moscow, the domestic market will not be in deep shock – there will be a slight decline in the profit of the Belarusian refineries, but a significant drop in supplies to Ukraine will not happen. In addition, Belarus is not a monopoly fuel supplier. Ukraine will be able to increase imports of fuel from other countries – such as Latvia, Poland and Russia itself (recently, Ukraine has significantly increased supplies of Diesel and LPG from the Russian Federation). At the time of the search for new suppliers in the market, a shortage of fuel can be created, which may lead to a short-term leap of prices.

Key players on fuel market

Is there really high fuel taxes in Ukraine?

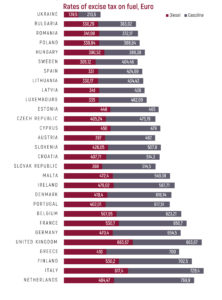

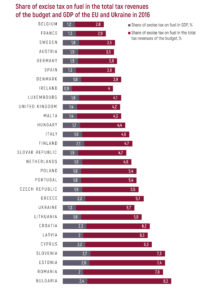

The rates of excise tax on fuel in Ukraine are much lower than in the EU countries – it concerns both gasoline and diesel fuel. Moreover, the share of taxes in the structure of prices in Ukraine is 35 % compared to 60% of the average European level.

However, the significance of excise tax revenue is comparable to average European indicators. As of 2016, the share of tax revenues from excise tax on total tax revenues from the consolidated budget of Ukraine was slightly higher than the average for EU countries (5.7% for Central European countries – 5.1%), while in relation to GDP it is lower ( 1.3% against 1.8% of average European level). But already in 2017, the excise tax on fuel in Ukraine grew by 43%, compared with 2016 and reached 1.8% of the country’s GDP. That is, they have reached the middle European level.

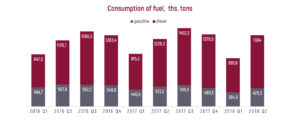

We expect that by the end of 2018 this trend will continue. Despite the general tendency to reduce fuel consumption in physical terms, it is possible to assume a slight increase in revenues from excise tax on fuel, compared with the previous year. This will happen at the expense of rising oil prices and lowering the hryvnia exchange rate. At the moment, 50% of the excise duty is paid to the state road fund, which is financing the construction of new roads.

The relatively low share of taxes in the price structure also determines the lower price of fuel compared to other EU countries.

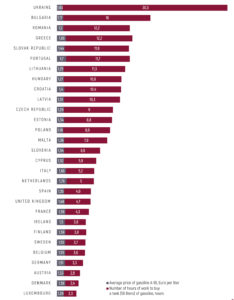

However, if you pay attention to how much time it takes to work an average Ukrainian, in order to pay a tank of gas, compared to the EU residents, it turns out that the relative price of gasoline in Ukraine is much higher. Thus, gas costs account for a much larger share in the expenditure structure of ordinary Ukrainians compared to the EU residents.

The price of fuel is included in the cost of almost all consumer goods in Ukraine. Therefore, while the income level of Ukrainians will be significantly lower than in European countries, Ukrainians will continue to be particularly sensitive to fuel prices.

Can domestic fuel production reduce the dependence on the currency factor?

Among the Ukrainians, it is commonly believed that if Ukraine had more gasoline of its own production, then they were less dependent on foreign exchange risks, which would not lead to such a price spike. And if its own gasoline were made from Ukrainian oil, then the price could be even lower. However, these assumptions are false.

In Ukraine today there are two petroleum product manufacturers: Kremenchuk Oil Refinery (Ukrtatnafta), controlled by Igor Kolomoisky, and Shebelinsky Gasoline Processing Plant (GPP) of the state-owned Ukrgazvydobuvannya (a group of Naftogaz of Ukraine).

10 more years ago in Ukraine there were 6 refineries – the already mentioned Kremenchug oil refinery, Lisichansk oil refinery (PJSC LINNIK), OJSC Lukoil-Odessky refinery, OJSC «Oil refining complex Galichina», OJSC «Petrochemical Prykarpattya», and OJSC Kherson-refinery . The total capacity of primary processing of these plants amounted to 51-54 million tons of oil a year (this exceeded similar capacities of Poland, Hungary, the Czech Republic and Slovakia taken together). The design capacity of these plants allowed not only to provide domestic demand for petroleum products, but also to export them to other countries. However, in practice these plants were always under-loaded. Among the reasons that led to the closure of 5 refineries – outdated equipment, poor quality of products, non-compliance with environmental standards and reluctance of Russian owners to develop fuel production in Ukraine.

However, despite the fact that there are only two factories operating in Ukraine, they occupy a considerable share of the petroleum and diesel fuel market. According to the results of the first half of 2018, the Kremenchug oil refinery occupied 36% of the gasoline market and 11.5% of the diesel fuel market, Shebelinsky gas processing plant – 6.4% and 1.5% respectively of the market. Moreover, both plants had problems with the sale of gasoline produced in the first half of 2018. One of the reasons is the poor image of Ukrainian fuel that has been formed for many years. This is especially true for Shebelink products. Kremenchug refinery sells the bulk of manufactured products through the network of gas stations, which also belong to Kolomoisky. Kremenchuk can sell fuel to other petrol stations, but in practice it is not so easy to implement. The reason is the image and specifics of the “Privat” management, which sometimes scares off potential customers – competing with “Privat” gasoline stations.

Both refineries work mainly on imported raw materials, which are bought for currency. Domestic oil extraction in Ukraine does not cover the needs of existing oil refineries. At the same time, Ukraine from 2007 to 2017 reduced oil production by half, although no specific cataclysms were observed. In addition, due to the uncompetitive and specific procurement market, oil in Ukraine is sold on the domestic market more expensive than in world markets. The margin of the refinery is insignificant, and the difference between the price of imported fuel and the purchase price of imported oil is about 10-15%. At the same time, the excise tax rates for fuel produced in Ukraine are the same as for the imported, that is fixed in the currency. Therefore, the price of fuel produced in Ukraine from imported oil is also dependent on currency fluctuations and prices on world markets.